Fiscal balance can be achieved by an aggressive fiscal policy: Results obtained by the use of the macro-econometric model.

Seiji Ono (Representative, Association for Japanese Economic Recovery)

Economy is recovered and the fiscal balance is achieved

We use the macro-econometric model, NEEDS developed by NIHON KEIZAI SHINBUN, NIKKEI and study the Japanese economy.

Let us consider the following scenario.

Scenario A

Large scale tax cut and public investment are assumed in this scenario. These are assumed to be additional fiscal spending to the ordinary policy in the way shown below. We studied various scenarios assuming various kinds of spending and we are going to show this one first. The additional fiscal spending is assumed to start from 2000.

(1) Public spending is assumed to be increased by 35 trillion yen every year.

(2) Corporation income tax is cut by the following amount:

| 20 trillion yen in 2000, 25 trillion yen in 2001, 25 trillion yen in 2002, |

| 25 trillion yen in 2003, 25 trillion yen in 2004 |

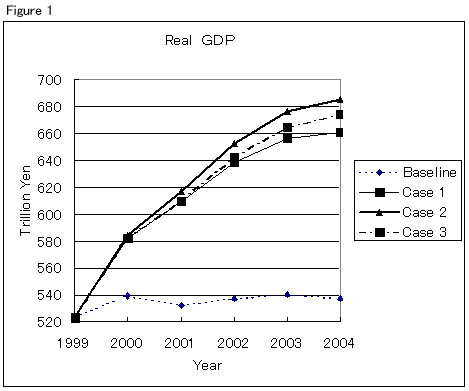

In Fig.1 temporal variation of real GDP is shown. In this kind of scenario many people worry about the drastic drop in the yen's value against dollar and/or about sharp rise in long-term interest rates. Thus, we show lines for the following three cases in addition to the baseline scenario, which means when present policy is kept.

| Case 1 | | Both yens value and long-term interest rates are assumed to be the same as those of baseline scenario. |

| Case 2 | | Yens value is assumed to drop as computed by the simulation and long-term interest rates are assumed to be the same as those of baseline scenario. This assumption leads to yens sharp depreciation. |

| Case 3 | | Both yens value and long-term interest rates are assumed to be computed by the simulation. In this case both drop substantially. |

As seen from Figure 1 a catastrophic drop in Japanese bond prices and/or in yens value affects the values of real GDP. It is extremely important to note that large scale additional fiscal spending recovers the economy remarkably whether Japanese bond prices and/or yens value drops catastrophically or not.

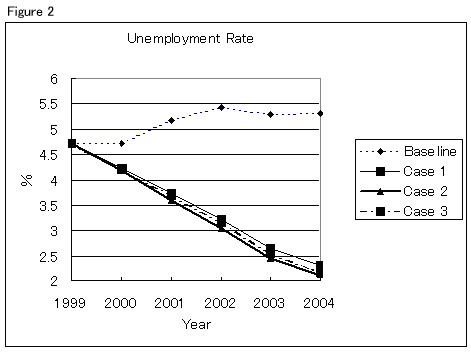

In Figure 2 the temporal change of unemployment is shown. The high unemployment rate lasts forever in the baseline while Case 1-3 shows sharp drop in unemployment rate. This again means rapid recovery of economy.

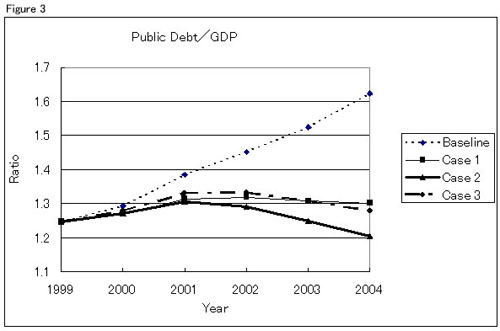

In Figure 3 the temporal change of public debt including local government divided by nominal GDP is shown. In the baseline this ratio increases constantly and reaches 1.62 in 2004 while this ratio stops increasing and start to decrease gradually in Case 1-3. In Case 2 the ratio drops to 1.20 in 2004. These results look surprising since government expenditure is increased a lot. These are related to the following facts (1) revenue from tax increases rapidly and the balance of payment improves substantially and (2) the increase of nominal GDP reduces the ratio.

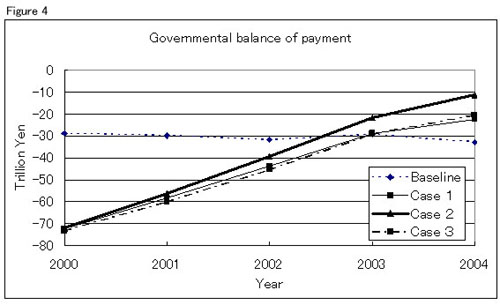

In Figure 4 we show the change in government fiscal balance. At the beginning of scenario A the deficit is huge, but it decreases rapidly and in 2004 the deficit is very little. The budget surplus might be achieved in one or two years. The first year, 2000, the deficit is huge but the increase of nominal GDP is also huge, thus this ratio becomes smaller in Case 1-3 than that in baseline.

Let us show some of the computed data of 2004 in Case 2 scenario A. The number in parentheses is the corresponding datum of the baseline:

Real gross domestic expenditure: 336 (301) trillion yen

Real private sector capital spending: 201(81) trillion yen

Current profits by corporation industry: 96 (32) trillion yen

Unit labor cost: 6,490,000 (4,960,000) yen/year

Unemployment rate: 2.11 (5.32)(%)

Governmental balance of payment: 11 (33) trillion yen

Total money supply: 942 (716) trillion yen

Nominal domestic housing investment: 19.7(16.4) trillion yen

Cash flow by corporate industry: 155 (87) trillion yen

Rate of operation (manufacturing) 91 (67) %

Nikkei stock average: 32,451 (8,324) yen

Index of urban land price: 55.0 (27.2)

Exchange rate of yen against dollar: 269 (120)

Balance of current account 22 (14.2) trillion yen

Balance of trade account 16.4 (10.6) trillion yen

Data in Cases 1 and 3 are not very different from that in Case 2. The consumer price index is as follows: 96 (baseline), 106 (Case 1), 113 (Case 2), and 111 (Case3).

We again confirm remarkable recovery of the economy in three cases (Cases 1-3). From Figures 1-4 and from the data above we can again confirm that it does not matter much whether or not Japanese bond prices and/or the yens value drops catastrophically. Note that many people oppose aggressive fiscal policy because of such drops.

Various improvements can be seen compared to the present policy (baseline) as a result of the aggressive fiscal policy:

Real GDP : 28% increase

Nominal GDP: 43% increase

Real Private sector capital spending: 2.5 times increase

Current Profits by corporation industry: 3 times increase

Unemployment rate: Decrease to 2.1%.

Inflation rate: 2.6%

Nikkei Stock Average: Increase to 32,000 yen.

Therefore, one can stop the deflation completely, thus bad loan problems will become much easier to solve and banking crisis is unlike to come again since banking business becomes profitable due to the large current profits by corporation industry. Concerning to the tax revenue in the baseline policy corporation income tax is 13.2 trillion yen, domestic income tax is 24.1 trillion yen, consumption tax is 11.9 trillion yen. Thus, these three amount to 49.2 trillion yen. On the other hand if the aggressive fiscal policy is taken, corporation income tax is 15.4 trillion yen, domestic income tax is 39.1 trillion yen, consumption tax is 16.4 trillion yen, that is, 70.9 trillion yen altogether. This means the increase of 21.7 trillion yen in the tax revenue. This is the revenue after the cut of 25 trillion yen of corporation income tax, thus if there is no tax cut the increase is as much as 46.7 trillion yen.

On January 20, 2003 Council on Economic and Fiscal Policy (CEFP) published a document named "Reform and Prospect". One can roughly say this is the future prospect of Japan by Japanese government. We call this "governmental prospect".

Governmental prospect

| Nominal GDP in 2010 | 584.6 trillion yen |

| Ratio of public debt to GDP | 1.21 times larger than that in 2002 |

| Unemployment Rate in 2010 | 4.4% |

Let us compare this with our prospect.

Prospect in aggressive fiscal policy. (Scenario A Case 2)

| | Nominal GDP | Ratio of public debt |

| | (Trillion Yen) | to nominal GDP |

| (After the start of | 1st year | 558 | 1 (definition) |

| this policy) | 2nd year | 586 | 1.06 |

| | 3rd year | 624 | 1.06 |

| Unemployment Rate | 1st year | 4.2% |

| | 2nd year | 3.6% |

| | 3rd year | 3.1% |

As seen from this comparison if aggressive fiscal policy is taken it takes only one or two years to achieve the governmental seven years target of GDP and unemployment rate. Furthermore, the ratio of public debt to GDP increases only 6% while in governmental prospect this increases 21% when achieved.

Scenario by strong tax cut

In the next place we consider the scenario when we stimulate the economy by strong tax cut.

Scenario B

[From 2001 to 2004]

(1) Corporation income tax is cut by 20 trillion yen.

(2) Domestic income tax is cut by 30 trillion yen.

(3) Consumption tax is totally cut, which means cut about 10 trillion yen.

Thus these three tax cuts is amount to altogether about 60 trillion yen per year. The first year, i.e., in 2000 the revenue is not enough for such huge tax cut. Thus the corporation income tax is cut only by 18 trillion yen and domestic income tax is cut only by 29 trillion yen. Anyway total amount of tax cut for five years is about 300 trillion yen (60x5).

Below is computed data from 2004 for Case 2, scenario B The number in parentheses is the corresponding datum of the baseline:

Nominal GDP: 668 (487) trillion yen

Real GDP: 680 (537) trillion yen

Real gross domestic expenditure: 373 (301) trillion yen

Real private sector capital spending: 181(81) trillion yen

Current profits by corporate industry: 88 (32) trillion yen

Unit labor cost: 6,400,000 (4,960,000) yen/year

Unemployment rate: 2.31 (5.32)(%)

Governmental balance of payment: 35 (33) trillion yen

Total money supply: 930 (716) trillion yen

Nominal domestic housing investment: 19.4(16.4) trillion yen

Cash flow by corporate industry: 144 (87) trillion yen

Rate of operation (manufacturing) 88 (67) %

Nikkei stock average: 27,892 (8,324) yen

Index of urban land price: 50.7 (27.2)

Exchange rate of yen against dollar: 280 (120)

Balance of current account 19.4 (14.2) trillion yen

Balance of trade account 12.1 (10.6) trillion yen

Data in Cases 1 and 3 are not very different from that in Case 2. Consumer price index is as follows: 96 (baseline), 101 (Case 1), 109 (Case 2), and 107 (Case3).

One can see again remarkable recovery of Japanese economy. These results are not much different from those of scenario A except that the improvement of governmental balance of payment is slower than that of scenario A. Scenario B turns Japan into paradise. Tax is drastically cut for five years, they can enjoy economic boom, and their income increases more than 20%. Inflation rate is low but deflation is gone away.

Public debt cannot be repaid by the increase in consumption tax.

Many people proposed the increase of consumption tax. Some of them insist to hike the consumption tax rate 1% every year until it reaches 16%. We show that public debt cannot be repaid by the increase in consumption tax.

Scenario S

The rate of consumption is raised 1% every year starting from 2000, i.e.,

| 2000 6%, | 2001 7%, | 2002 8%, | 2003 9%, | 2004 10% |

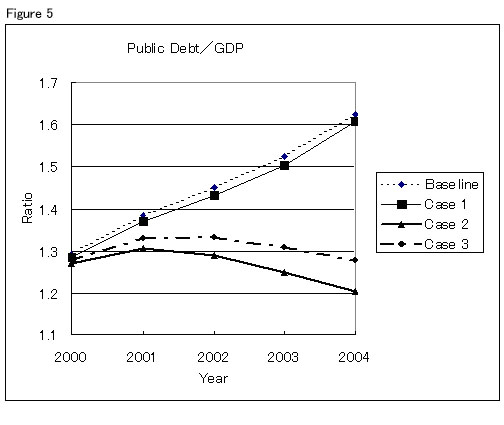

We call this Case 1. Yens value is assumed to drop as computed by the simulation and long-term interest rates are assumed to be the same as those of baseline scenario. As for Case 2 and Case 3 we use those for scenario A. The results are shown in Figure 5, which clearly shows that one can never repay the public debt in this way. One the other hand the aggressive fiscal policy can "repay" the public debt to a certain extent (Case 2,3).

To make the matter worse tax hike weakens the economy further, accelerating the deflationary spiral. Real GDP decreases 3.5%, current profits by corporation industry decreases 20%.

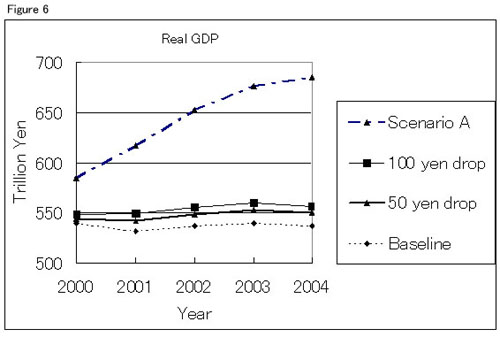

How effective is the policy of letting the yen fall in value on foreign exchange markets?

We study the following two possibilities.

Scenario S

| (1) 50 yen drop: | The exchange rate of yen against dollar is lowered by 50 yen. |

| (2) 100 yen drop: | The exchange rate of yen against dollar is lowered by 100 yen. |

The results are shown in Figure 6. One can see from this figure that the yen fall contribute to boost the economy only a little. Strong fiscal policy is more than 10 times effective as seen in this figure. Furthermore the policy of letting the yen fall in values drastically will inevitably cause trade conflicts.

Acknowledgements

The author would like to thank Professor Shuntaro Shishido, Professor Paul A. Samuelson, Professor Lawrence R. Klein, and Professor Haruki Niwa for their comments, communications, and discussions.

|